ISHAQ KUNDAWALA

Professor of Law & Southeastern Bankruptcy Law Institute and W. Homer Drake, Jr.

Endowed Chair in Bankruptcy Law, Mercer University School of Law. B.A., Austin College; J.D.,

Tulane Law School.

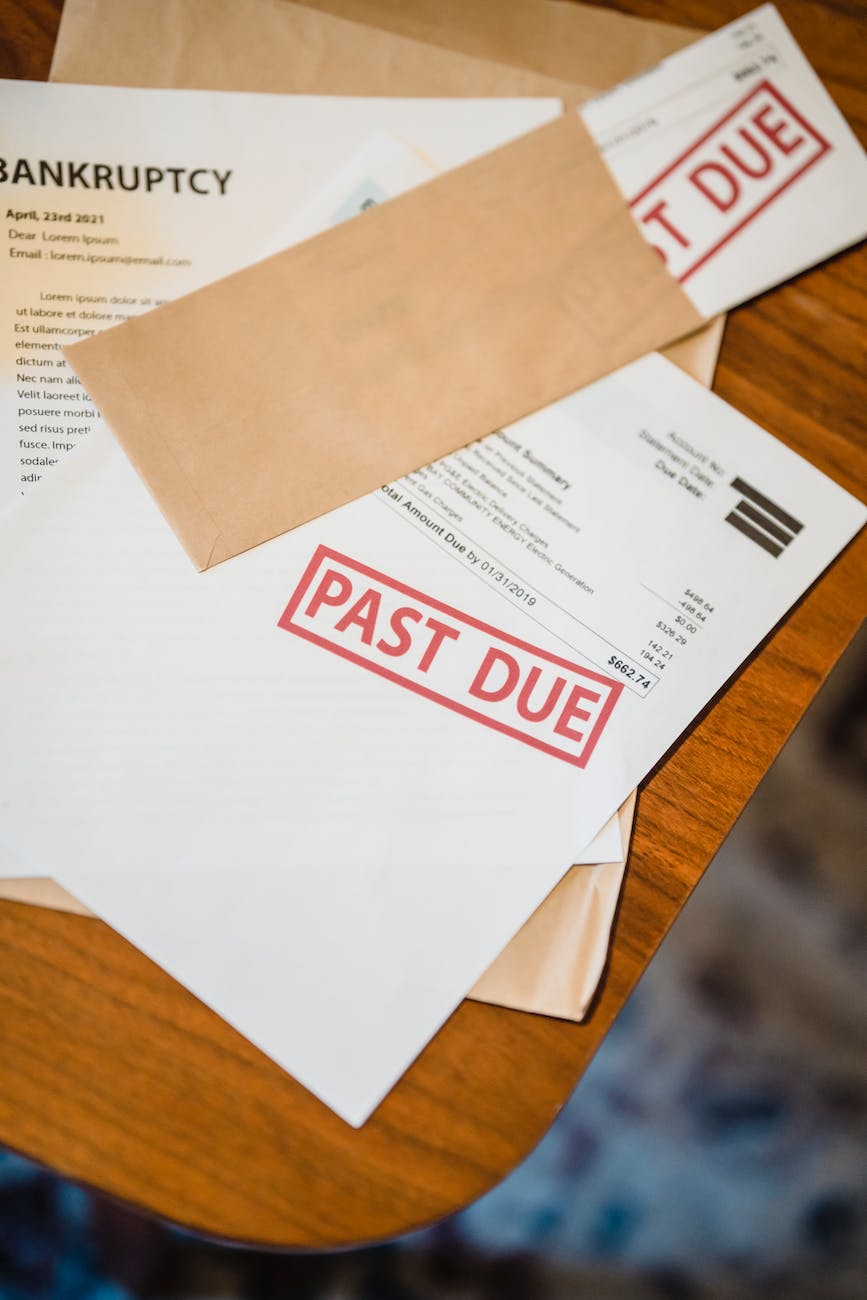

Imagine an individual who is too broke to file for bankruptcy relief. This irony is far too often a reality in America, especially for people living in underserved communities. Debtors are simply unable to skimp and save up even a thousand dollars to pay their bankruptcy attorney. Paying their bankruptcy attorney upfront in full is the only ticket to seeking Chapter 7 bankruptcy relief.

For a variety of reasons, Chapter 7 bankruptcy relief is the most advantageous type for a majority of poor and middle-class individuals and families. It provides these individuals and families with an expedient, fresh financial start in life. In fact, this fresh start is one of the main reasons our bankruptcy system exists.

Without access to funds to pay their attorney, these folks have only one option when it comes to bankruptcy relief; and having one option is not a choice—it is a mandate. These individuals are left to file a Chapter 13 bankruptcy case, which allows for the payment of a debtor’s attorney in postpetition installments over time, usually three to five years. It is certainly an option, but likely not the best one, and it is far more expensive than a simple Chapter 7 bankruptcy.

Read Professor Kundawala’s entire article here .